Interpreting recent productivity performance in Canada

Exploring why productivity has been decreasing recently

Strong productivity growth is widely considered a crucial characteristic of the modern dynamic economy. It brings increases in real household incomes that can compound over the years and it implies that an economy is flourishing. An economy without productivity growth, if the situation continues, faces stagnation.

In this light, there is much concern about the poor performance of Canadian labour productivity in recent years. This short article explores the reasons for this poor performance.

Picturing Canada’s productivity performance

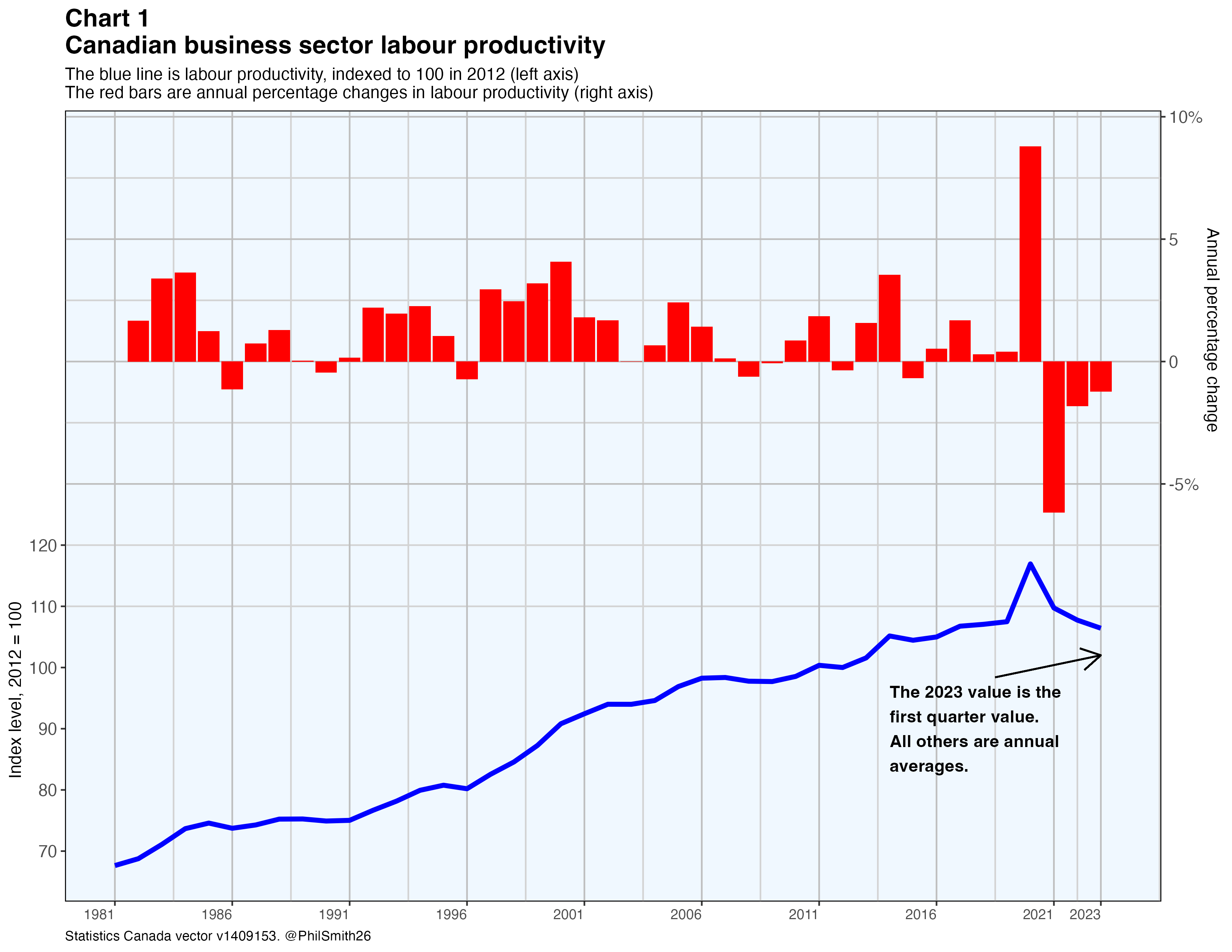

Chart 1 is a picture of Canadian business1 labour productivity since 1981. The blue line represents productivity itself — the amount of real business sector output produced in a given year per hour of labour services used to produce it. The line covers a 41 year period and increases at a 1.1% compound annual rate. The rates of increase or decrease in individual years are shown as red bars.2

If one compares the 28-year period extending from 1981 to the end of the ‘Great recession’ in 2009 to the subsequent 10 years ending in 2019, average annual productivity growth decreased from 1.3% to just 1.0%. This was concerning. But the results in the pandemic-affected years 2020-2023 have been more troubling. The level of productivity in the first quarter of 2023 was 1.0% lower than it was before the pandemic in 2019.

Causes of the recent productivity downturn

To understand the recent labour productivity downturn, it is helpful to adopt the decomposition used by Statistics Canada in its annual productivity accounts.3 These accounts offer a detailed statistical framework that takes account not just of labour services inputs, but also of capital services inputs, and does so with allowance being made for different types of capital services and labour services. The labour productivity measure referred to in the previous section, which is the one most commonly seen in current economic analyses, makes no explicit reference to the capital services input and treats the labour services input as if all hours worked are equivalent, whether by an unskilled and inexperienced worker earning minimum wage, or by a highly trained and experienced professional earning a six- or seven-figure annual income.

In the productivity accounts, the annual percentage change in labour productivity as conventionally measured is decomposed into three components which are:

Multifactor productivity (MFP) growth, which is the change in output in a given year that cannot be attributed to changes in the the quantities of labour and capital services inputs used in production. This is the increase in productivity resulting from technological change, alterations in the way production processes are organized and changes in the scale of production.

The change in labour composition, which is the extent to which the total labour services input, measured as the count of hours worked, reflects more or less skilled and experienced workers than in the previous period. The productivity accounts break down the labour input into 56 components with different skills and experience, and weight each by its share of labour compensation.

The change in capital intensity, which is the extent to which the quantity of capital services available per hour of labour services is greater or less than in the previous year.

In mathematical notation:4

Δln(LP) = Δln(MFP) + sk * (Δln(K) - Δln(H)) + sl * (Δln(L) - Δln(H))

In words, the relative change in labour productivity as conventionally measured (LP) is equal to the relative change in MFP plus the relative change in capital services (K) less the relative change in total hours worked (H), all weighted by the share of capital in total factor income (sk), plus the relative change in labour services (L) less the relative change in total hours worked (H), all weighted by the share of labour in total factor income (sl). This decomposition allows us to see the annual change in labour productivity, conventionally measured, as the net result of multifactor productivity growth, increases or decreases in the amount of capital services made available to complement the labour services input, and upgrading of labour skills and experience.

Multi-factor productivity growth

Chart 2 shows estimated multi-factor productivity (MFP) and its annual growth rate since 1981. Note that it is calculated indirectly as a residual — the difference between measured output growth and the weighted sum of the growth of the associated labour and capital service inputs.

As can be seen, MFP has been trending up since the end of the 2008-2009 recession, growing at a 0.6% compound average annual growth rate between 2009 and 2020 before dropping in 2021. MFP, as estimated, appears to be quite cyclical and the sharp pandemic-related downturn in the economy in the spring of 2020 may explain the decrease in MFP in 2021.5 Statistics Canada’s estimates for 2022 are not expected to be available until the spring of 2024.

Labour quality

As noted, the productivity accounts measure the labour services input as a weighted sum of 56 hours-worked components. Using data from the Labour Force Survey, the Census of Population and other sources, hours at work are tabulated for 4 classes of educational attainment, 7 classes of work experience and 2 classes of workers (4 x 7 x 2 = 56). The two classes of workers are employees and the self-employed.

The labour services input is defined as the sum of all 56 hours-worked variables, each weighted by its factor compensation. The labour services input variable can then be interpreted as labour services per hour worked (a ‘labour composition’ variable) times total hours worked (the conventional labour input variable). In other words, in this formulation the labour services input measure is quality-adjusted.

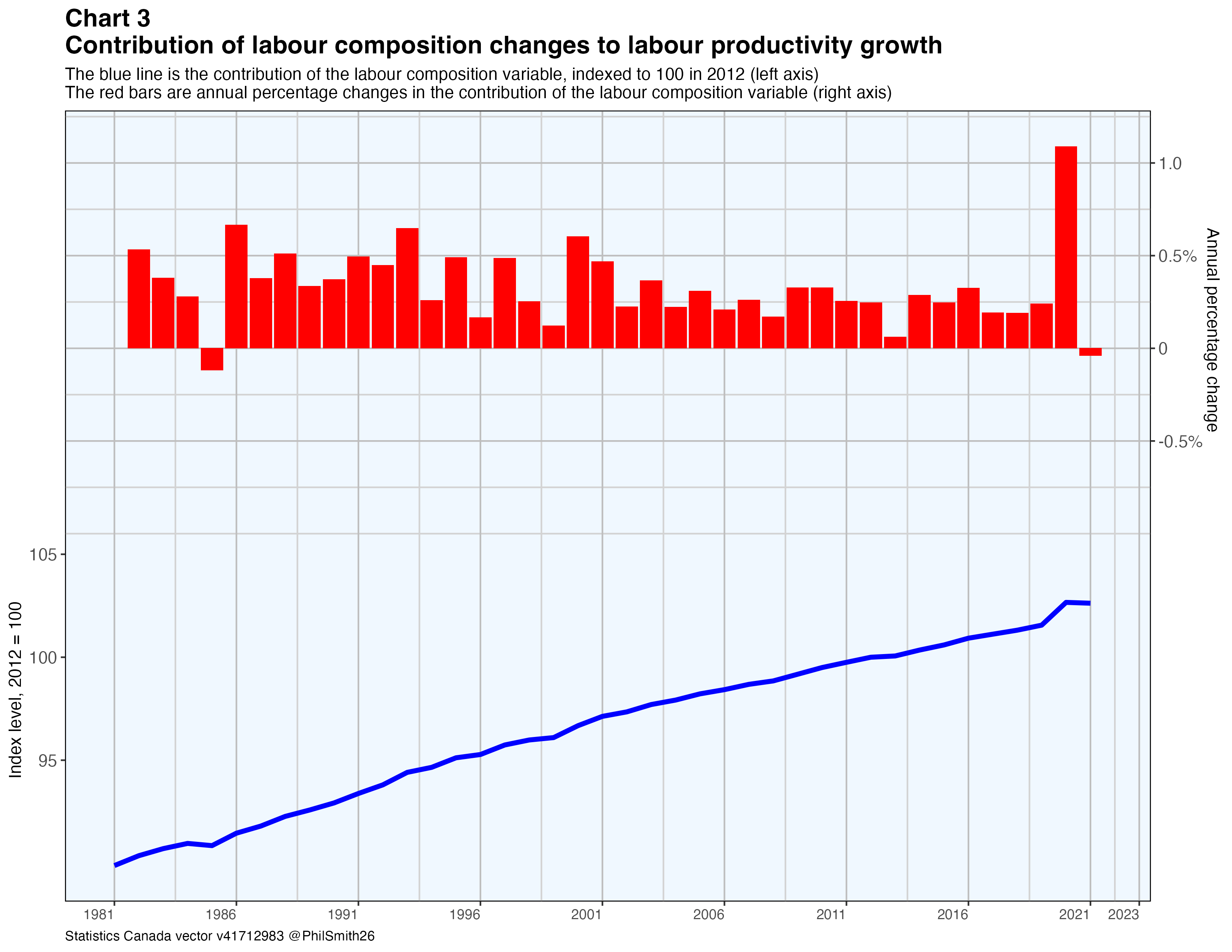

Chart 3 shows the contribution of the labour composition variable to labour productivity growth between 1981 and 2021. It is evident that annual labour quality upgrading tended to be somewhat greater up to around 2001 and has been somewhat less since then. This may be due in part to demographic factors. The compound average annual increase was 0.4% in the first of these periods and 0.2% in 2010-2019.

In 2020 labour composition improved greatly, but not because of a sudden surge in the education and experience of employees. Rather, it was mostly a temporary compositional effect from the pandemic restraints. Layoffs due to the pandemic, viewed as temporary, tended to be focussed on less educated and experienced people, while firms ‘hoarded’ their more difficult-to-replace skilled employees. As a result, the average quality of an hour of labour services increased substantially.

In 2021, the labour composition variable decreased, but only slightly as many of the layoffs continued, especially in the public-facing services sector. Although as mentioned no estimates are presently available from Statistics Canada for the labour composition variable in 2022, we can expect it to have decreased also in that year and probably more substantially as the economy got back to normal and firms rehired lower-skilled and less experienced employees.

Chart 4 compares the conventional measure of the labour input — the count of hours worked — with the quality-adjusted measure. The former grew at a 2.1% compound average annual growth rate over the full period while the latter increased 3.1%, so clearly labour quality upgrading has been a consistently important factor in raising labour productivity.

Capital intensity

Capital intensity is the amount of capital services — the services provided by capital assets such as machinery and equipment, structures and intellectual property products — made available per unit of labour services for use in production activities. Capital services clearly augment the productivity of labour.

Statistics Canada’s productivity accounts measure capital services by decomposing the capital stock of the business sector by type of asset. Some types, such as most structures, are expected to have relatively long lives while others, such as many types of machinery and equipment, have shorter lives.

The services available from a given item of capital in a given year depend on its expected lifespan. For example, if depreciation is linear a $100 capital asset with a 10-year lifespan will be expected to contribute $10 of capital services per year while a $100 asset with a 50-year lifespan will contribute only $2 of capital services per year.6 Summing over the different types of capital asset, Statistics Canada derives an estimate of the real value of capital services provided to production by the capital stock in a given year.

The contribution of capital intensity to labour productivity growth is calculated as the growth in capital services per hour worked times capital's share of total costs. It reflects the effects of capital investment on labour productivity growth. Chart 5 shows the contribution of changes in capital intensity to changes in labour productivity.

Over the period from 1981 to 2019, before the pandemic, capital intensity rose at a compound average annual rate of 0.8%. This growth depends, of course, on the amount invested in new capital goods each year by businesses and on the composition of that investment by expected lifespan, as well as the depreciated value of previously accumulated capital. The pace of investment was a lot stronger in the 28-year period from 1981 to 2009, when the contribution of capital intensity grew 1.0% per annum, than was the case in the subsequent 10 years to 2019 when capital intensity rose only 0.4% a year.

Chart 6 shows real business investment in four major categories. The blue line, for engineering construction, is dominated by oil-and-gas-related investment, including pipelines. It increased strongly from 2009 to 2014 and then declined up to 2020 as world energy prices declined. It recovered, although only slightly, in 2021 and 2022 when global energy prices began to rise again. While this kind of investment is the largest in dollar terms, it also has long lives7 so its annual contribution to labour productivity growth or decline is relatively small. The same is true for non-residential building construction, the red line, although in this case the annual level of investment in volume terms since 2009 has been fairly stable.

Machinery and equipment investment typically has a shorter expected life than construction investment,8 so a dollar of this investment contributes more to changes in labour productivity. This kind of investment is cyclical and it increased from 2009 to 2014 before decreasing in 2015 and 2016 during Canada’s ‘mini-recession’. It increased again in 2017-2019, fell in the COVID-19 year of 2020, and then increased modestly in 2021 and 2022.

Intellectual property product investment is also relatively small and its estimated annual depreciation rates are high. The rate for software is 55%.

Interpretation of recent labour productivity developments

The published productivity estimates for 2010-2021 and some estimates for 2022 and 2023 are summarized in table 1 below. They indicate that MFP increased 0.7% in 2020, not much different from the 2009-2019 average annual growth rate of 0.6%, and then plunged -2.1% in 2021. Labour productivity rose 8.6% in 2020 before dropping 5.9% in 2021 while capital productivity decreased 7.1% in 2020 and then rose 3.3% in 2021. How are these findings to be interpreted?

As is well understood, 2020 and 2021 were extraordinary years for the economy. Labour productivity, as conventionally measured, increased very greatly in 2020 and this was clearly due mostly to the changed composition of the workforce, rather than to accelerated employee training or enhancements to the capital services employees work with. As previously noted, employers disproportionately laid off lesser-skilled and lower-paid employees during the pandemic shutdowns. Then in 2021 the decrease in labour productivity primarily reflected the partial return toward normality in this composition. Capital productivity behaved in an opposite fashion because unlike labour services, capital services were not generally “laid off” during the pandemic shutdowns. Since output declined in 2020 and then rose again in 2021, while the capital services input did not change all that much, capital productivity moved much like output. Capital intensity, on the other hand, increased greatly in 2020 and fell back somewhat in 2021.

The growth pattern for MFP in 2020 and 2021 is more difficult to explain. However we know it tends to be cyclical — see chart 2 — and this is perhaps the explanation. MFP rose 0.7% in 2020 on the heels of an upward cyclical movement in output between 2010 and 2019 and then fell substantially in 2021 following the sharp economic drop in the spring of 2020. As mentioned earlier, one can hypothesize that entrepreneurs are more likely to pursue MFP-enhancing innovations when an economic expansion is under way and they are not in “naked survival mode”.

In summary, the labour productivity growth pattern of 8.6% in 2020 and -5.9% in 2021 can be decomposed as the sum of (1) MFP growth of 0.7% and -2.1% in the two years, (2) labour composition upgrading of 1.9% and -0.1%, and (3) contributions from capital intensity changes of 6.7% and -3.9%.

While we do not know what the full suite of productivity statistics for 2022 and 2023 will be, since Statistics Canada will not estimate them until 2024 and 2025, table 1 includes a scenario put together by the author. We do have some information about 2022 and 2023, of course, and the estimates reflect this information. For example, we know that business sector real GDP increased 3.8% in 2022 and that it has been increasing more slowly so far in 2023. We also have estimates of hours worked for 2022 and the first seven months of 2023. We have estimates of total labour compensation and capital cost in 2022 from Statistics Canada’s income and expenditure accounts and preliminary estimates for the first quarter of 2023. Finally, quarterly estimates of business sector investment, depreciation and capital stock are available in Statistics Canada table 34-10-0163-01, albeit without much detail by type of capital. Putting all of this information together yields the 2022 and 2023 estimates in table 1.

In this scenario labour productivity continues to decrease in 2022 as the re-employment of previously-laid-off lower-skilled workers continues and the composition effect that started in 2020 is fully reversed. Labour productivity then rebounds with a relatively strong 1.7% increase in 2023. This pattern in the two years reflects the following additive components: (1) increases of 1.8% and 0.4% in MFP as entrepreneurs resume their pursuit of profit-enhancing innovations as the economy booms in 2022, (2) a decrease in overall labour quality of -1.4% in 2022 as businesses struggled to find the labour they required in a hot labour market followed by a positive contribution to labour productivity from labour upgrading in 2023 when labour markets had calmed down somewhat and (3) a second decrease (-2.1%) in the contribution to labour productivity from capital intensity changes in 2022 as the labour composition disruption in 2020 continued to unwind, followed by a return to a positive capital intensity contribution of 0.6% in 2023.

The bottom line here is that while the pattern of labour productivity growth seen in 2021 and 2022 might look frightful, most of it can be explained by the compositional shifts that occurred during the first year of the pandemic and were gradually unwound in the two subsequent years, combined with a slowdown of business investment and the apparent tendency of MFP improvements to decrease temporarily when a significant economic decline occurs. We have good reason to expect stronger labour productivity growth in 2023 and the years thereafter now that the pandemic-induced distortions are unwound.

The focus on productivity is limited to the business sector because there are no reliable estimates available for the government and non-profit sectors. The difficulty for the latter is that there are no market prices for most of the sector output. Without market prices for, say, elementary school education or government administration services it is impossible to calculate reliable estimate of real output, the numerator of the productivity calculation. As a result, statisticians typically assume that real output is proportional to the real labour input, hours worked, which implies an assumption of constant labour productivity over time. Unfortunately there are no systematic estimates of the productivity of government employees.

This is Statistics Canada’s quarterly measure of labour productivity, released in their table 36-10-0206-01. The quarterly estimates are converted to annual in this article by averaging within each year. The agency also releases a more detailed but less timely set of annual productivity estimates in table 36-10-0208-01, which are discussed in the next section of this article.

The productivity accounts are explained in a paper by John Baldwin, Wulong Gu and Beiling Yan, of Statistics Canada. The statistical estimates for these accounts cover the period 1961 - 2021 and are available in Statistics Canada table 36-10-0208-01. These statistics are based on the supply and use tables, which provide a very detailed and internally consistent set of estimates of outputs and inputs in the Canadian economy, by product group, by industry and by province and territory. The estimates cannot be made available quickly, since it takes a considerable amount of time for the necessary data sources to become available so the supply and use tables can be constructed. But they are the gold standard when it comes to interpreting Canadian productivity changes. The statistics became available for the year 2021 on April 18, 2023. They allow us to explore, in detail, what happened to the productivity of Canada’s business sector when the pandemic struck in 2020 and in the subsequent year when the economy started to recover.

A detailed mathematical presentation of the productivity accounting framework is available in the paper referenced in footnote 3.

It can be hypothesized that the entrepreneurial forces leading to the innovations that cause MFP to increase are weakened during economic downturns, when businesses are focussed more on survival in the face of lower demand for their products.

Linear depreciation is the adopted assumption for purposes of this example, although Statistics Canada also provides estimates based on hyperbolic and geometric assumptions. The point being made holds true regardless of which assumption is used. Statistics Canada’s productivity accounts use the geometric depreciation assumption.

For example, in the productivity accounts geometric depreciation rates of just 7% for downstream oil and gas engineering facilities, 13% for upstream oil and gas engineering facilities and 8% for other engineering construction are assumed. Office buildings have a depreciation rate of just 0.6% and passenger terminals and warehouses 7%.

Some examples for machinery and equipment depreciation rates are 47% for computers, 24% for office furniture and 28% for automobiles.

A very interesting analysis Philip. I hope it gets the attention it deserves from officials and elected decision makers and illuminates their policy decisions so that they can steer the country towards much needed greater productivity and innovation.